Given its geographic position, abundant natural and agricultural resources, and moderate labor costs, Colombia has the potential to develop a competitive chemicals industry, as long as it is committed to the necessary investment and research.

Well-known for its coffee exports, Colombia also has an advantageous geographic location, significant mineral and energy resources, diverse agricultural products, and reasonable labor costs — all of which provide a good foundation for the country’s chemical process industries (CPI). Hydrocarbon refining and processing; coal, gold, and ferronickel mining; cement production; and chemical and pharmaceutical manufacturing form the industry’s backbone. Food, beverage, and consumer products production are also important to Colombia’s economic growth and employ many chemical and process engineers.

This article provides an overview of Colombia’s chemicals industry and associated industries, and discusses the history, economy, and future of these sectors.

Industry overview

▲Figure 1. Colombia’s Caribbean (blue), Orinoquía (yellow), Andean (purple), and Pacific (orange) regions are home to most of the country’s chemical process industries. The Amazon region (green) is known for its tropical rainforests.

Colombia is roughly equivalent in size to New Mexico, Texas, and Louisiana combined. A unitary republic with 32 departments and a capital district, the country can be divided into five distinct geographic areas: the Andean, Caribbean, Pacific, Orinoquía, and Amazon regions (Figure 1). The Caribbean, Andean, Orinoquía, and Pacific regions are home to most of Colombia’s chemical production facilities. The Andean region has the highest concentration of industrial plants, while most oil production occurs in the Orinoquía region, which borders Venezuela.

Coal mining, petroleum production and refining, and beer production are important industries in the Caribbean region. Open-pit coal mining is based in the region’s Cesar and Guajira departments, while the port city of Santa Marta exports coal. Petroleum is processed at the Reficar refinery in Cartagena, and petroleum derivatives are produced at the Monómeros Colombo Venezolanos chemicals facility in Barranquilla. SABMiller, a multinational brewing and beverage company, has a significant beer production plant in Barranquilla.

The Andean region is the most urbanized and industrially developed. In the Antioquia department, cement, chemical, and food and beverage production are concentrated in the city of Medellín. Grupo Nutresa, a leading producer of processed foods in Latin America, has a facility in the city, as does Grupo Orbis, the country’s paint and chemical products conglomerate. Postobón, Colombia’s largest beverage company, and Grupo Argos, the region’s largest cement producer, also have industrial works in Medellín.

Elsewhere in the Andean region, Ecopetrol processes oil at Barrancabermeja, the country’s largest oil refinery, which is supplied with 10,000 barrels per day (bpd) of crude from Infantas oil field, 4,000 bpd from the Provincia field, and 2,000 bpd from the Llanito field (1). Argos and Holcim, two dominant players in the Colombian cement industry, have production facilities in the Boyacá department, while in the capital city of Bogotá, Carboquímica’s plants supply raw materials for plastics and polyvinyl chloride production. Food and beverage and personal care manufacturers also have operations in the region. SAB Miller PLC has breweries in both Boyacá and Bogotá, and Belcorp Corp. and Quala S.A. produce cosmetics and personal care products in Bogotá.

Pacific region activities are centered in the Valle del Cauca department, where processed meats, refined sugar, and personal care products are promising industries. Crude oil production drives the Llanos region’s chemical industry, with the Quifa oil field yielding 56,000 bpd; the Rubiales field, 163,000 bpd; the Castilla field, 125,000 bpd; and the Chichimene field, 80,000 bpd (1).

History and key companies

Colombia’s chemicals industry started in the 1940s with the creation of the Institute for Industrial Promotion (Instituto de Fomento Industrial, IFI). Chartered to promote key industrial sectors, IFI supported the National Chlorine and Derivatives Co. (Compañía Nacional de Cloro y sus Derivados), which was founded in 1942 (2). The chlorine industry developed rapidly in the Andean municipalities of Betania in Antioquia and Zipaquirá in Cundinamarca with construction of Colombian Soda Plant’s (Planta Colombiana de Soda) production facilities. Now known as Brinsa, the company maintains production facilities in Cartagena (Caribbean region) and Zipaquirá (Andean region).

As the country’s agricultural sector developed in the 1960s, demand for fertilizer grew, spurring growth in the chemicals sector. In 1967, the Colombia and Venezuela governments jointly created Monómeros Colombo Venezolanos, which built a caprolactam and compound fertilizer production plant in Barranquilla. This company is now controlled by Venezuela Petrochemicals (Pequiven). In 1956, Carboquímica had begun to produce aromatic solvents in Bogotá and, by 1962, expanded the facility to produce phthalic anhydride. The company continued to expand, opening a synthetic resins production facility in 1974. Today, Carboquímica is one of the leading Colombian companies in this chemical industry sector (2).

In the oil sector, Ecopetrol (Empresa Colombiana de Petróleos) was established in 1948 as a state-owned enterprise. In a historic event, Ecopetrol took over the International Petroleum Company’s Barrancabermeja refinery, operational since 1922 (3). In 2007, Ecopetrol became a mixed corporation, with 80% of stock owned by government and 20% held privately. In 2015, Ecopetrol’s new Reficar refinery began operations in Cartagena. It was initially conceived as an extension of an existing location. During facility construction, however, process specifications were modified so that the refinery could process heavier crude (18° API gravity). Reficar and Barrancabermeja today have the combined capacity to refine approximately 415,000 bpd.

Colombia produces about 1 million bpd of oil. According to the International Energy Agency (IEA), the country ranks as the 19th largest oil producer in the world and the fourth largest in Latin America after Brazil, Venezuela, and Mexico. Colombia is not a top crude oil refiner in the world or Latin America, ranking fifth in Latin America after Brazil, Mexico, Venezuela, and Argentina. The country had proven crude reserves of 2,300 million barrels as of 2014, enough to process and sell for about six years at current rates of exploitation.

As the Colombian consumer-product industry developed, alcoholic and nonalcoholic beverage production increased (2). Commercial beer production began in 1913 with the opening of the Águila Brewery in Barranquilla, followed in 1930 by the Bavaria Consortium in Bogotá. Bavaria acquired Águila in the 1970s and became Colombia’s largest beer producer. In 2005, Bavaria was acquired by SAB Miller PLC. Carbonated beverages are primarily produced in Medellín by Postobón, which was created when the Posada and Tobón families merged their companies. Postobón is now one of the country’s leading private companies, with a large product portfolio of soft drinks, fruit juices, bottled water, tea, and energy drinks.

Colombia does not have large basic-chemicals companies; however, it does have several consumer products companies with international presence. NOEL, a major producer of Colombian cookies, was founded in Medellín in 1916. Since 2005, it has been part of the Nutresa Group, a conglomerate of Colombian companies that produce cookies, ice cream, meat, chocolates, fast food, coffee, and pasta. The National Chocolate Co., a privately held producer of chocolate and chocolate products, was founded in 1920 in Medellín. The company became part of the Nutresa Group in 2009.

The Institute for Industrial Promotion (IFI) was instrumental in promoting the Colombian milk industry in several regions (2). INDUCOLSA, founded in 1952 in Valle del Cauca, is now known as Industria Colombiana de Alimentos. Privately held Alpina was founded in the 1940s in the Andean region and has become a dairy sector leader. The COOLECHERA cooperative was founded in 1964 in Antioquia and is now called COLANTA. One of Alpina’s biggest competitors, COLANTA has approximately 7,000 associates and 12,000 producers (4).

Chemical industry economics

Total gross sales for the Colombian CPI, including consumer products and food and beverage industries, were $70.75 billion in 2014, which represents almost 19% of the country’s gross domestic product (GDP) of $378 billion, at current prices. Total gross sales, minus intermediate consumption, represent an added value of $26.6 billion. The National Manufacturing Survey (Encuesta Nacional Manufacturera), which evaluates the economic and productive performance of the country’s largest industrial enterprises, consolidates data for Colombia’s manufacturing industries (5). The survey only considers production activity. Mining, and activities where marketing adds value, are considered separately.

When industrial sales of processed food and plastic products are subtracted from total gross sales, the chemical sector represents $49 billion (13% of GDP), of which $22.8 billion correspond to petrochemical products. Bioethanol and biodiesel fuel production sales account for $650 million in sales. Refined petroleum products and consumer products, such as food, beverages, and personal care products, account for over half of the industry’s sales. Table 1 shows percentages of total gross sales for each of the main industrial chemical sectors.

| Table 1. The 2014 percentages of gross sales for various sectors of Colombia’s chemical industry (5). | |

| Sector | Percentage |

| Refined petroleum products | 31.8% |

| Other chemical products | 9.6% |

| Beverages | 8.9% |

| Production of other food products | 7.1% |

| Nonmetallic mineral products | 7.1% |

| Plastic products | 5.8% |

| Basic chemicals, fertilizers, plastics, and synthetic rubber | 5.2% |

| Dairy products | 5.0% |

| Paper, cardboard, and paper products | 4.9% |

| Iron and steel | 4.2% |

| Animal feed | 3.8% |

| Pharmaceuticals, medicinal chemicals, and botanicals | 3.6% |

| Precious metals and nonferrous metals | 3.1% |

| Based on $70.75 billion in gross sales with value added to GDP of $26.6 billion for 2014. | |

The mining industry represented an added value of $31 billion in 2014. When compared to the industry’s $26.6 million, it shows the Colombian economy’s strong dependence on its mining sector.

Employment. Colombia’s CPI sectors, represented in Table 1, provide about 270,000 of the 582,000 manufacturing jobs available in 2014. More than 90,000 jobs were in the processed food industry.

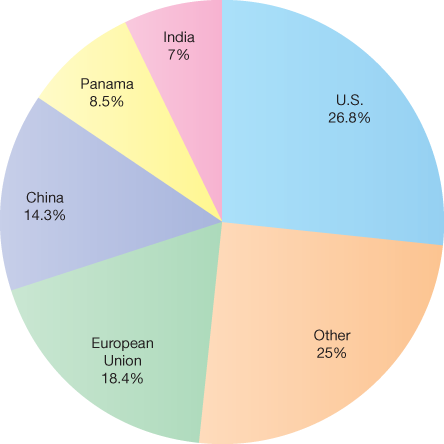

▲Figure 2. Mining products, such as coal and gold, account for about 70% of Colombia’s exports, which are shipped to the U.S., the European Union, and China, among other countries.

Exports. Colombia registered exports of $54.8 billion in 2014, with a strong dependence on mined products. The country exported 314 million bpd of crude oil, 89,085 ton/yr of coal, and 48.1 ton/yr of gold, representing 70.1% of total annual exports. Figure 2 shows Colombia’s top export destinations for mining commodities and crude oil, including the U.S. (26.8% of exports), the European Union (18.4%), and China (14.3%) (6).

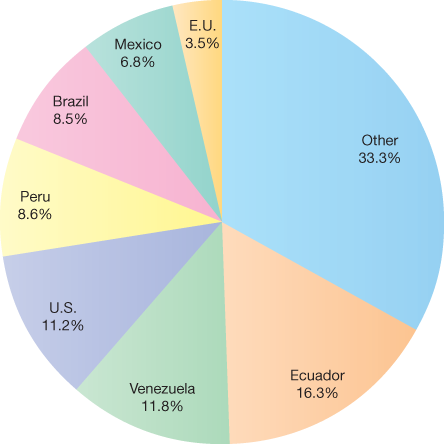

▲Figure 3. Colombia exports various chemical products to countries including Ecuador, Venezuela, and the U.S.

Colombia exports chemical products to many countries (Figure 3), including Ecuador (16.3% of exports), Venezuela (11.8%), and the U.S. (11.2%). Table 2 summarizes the country’s top chemical exports for 2014 (6). Pharmaceuticals accounted for about $450 million in exports, followed by propylene polymer ($392 million), and vinyl chloride ($324 million).

| Table 2. Colombia’s top chemical exports in 2014 (6). | |

| Product | Sales, $U.S. MM |

| Pharmaceuticals | 449.7 |

| Propylene polymer | 392.6 |

| Vinyl chloride | 323.6 |

| Cosmetics | 163.9 |

| Styrene | 110.3 |

| Soaps | 106.8 |

| Fragrances | 102.9 |

| Batteries | 99.0 |

| Mineral fertilizers and other chemicals | 98.8 |

Corporate Sales. The 2014 gross sales for Colombia’s leading companies are listed in Table 3(7). Ecopetrol, for which the Colombian state is the largest shareholder, reported total sales of about $29 billion, followed by Bavaria with $2.3 billion in beer sales, and Drummond with $1.6 billion in coal revenues.

| Table 3. Total sales for Colombia’s principal chemical companies in 2014 (7). | ||

| Company | Chemical Sector | Sales, $U.S. MM |

| Ecopetrol | Oil refining and crude oil | 29,000 |

| Bavaria | Beer | 2,253 |

| Drummond | Coal | 1,610 |

| Colanta | Dairy products | 938 |

| Esenttia | Plastics | 819 |

| Organización Soila | Animal feed | 758 |

| Colombina | Confectionery | 649 |

| Cerro Matoso | Ferronickel | 655 |

| Tecnoquimicas | Pharmaceuticals | 610 |

| Colgate Palmolive | Personal care products | 578 |

| Mexichem Resinas de Colombia | Plastic products | 494 |

| Diaco | Iron and steel | 483 |

| Smurfit Kappa | Cardboard and paper | 399 |

The future

Colombia does not have a highly developed chemicals industry. Between 2008 and 2014, high global prices for minerals and petroleum favored the development of these sectors at the expense of others. In 2014, however, with falling international prices and the devaluation of the peso, Colombian leadership realized that the country could not concentrate all its efforts and investments on oil and mining. Colombia then began to develop its production capabilities for consumer products such as food, drinks, toiletries, and cosmetics. Moving forward, these products will provide significant added value to the nation’s economy.

When global prices are again favorable, mining will likely offer economic development opportunities for Colombia. The industry, however, needs to address the environmental and social impact of illegal gold mining activities. The effects left by nonregulated exploitation are substantial, and inhibit the country’s social development.

Colombia invested heavily in Reficar’s construction, which eventually cost $8 billion. While the country’s investment promises to increase the value of the chemical industry, value creation depends on reaching projected production levels, and doing so efficiently. Colombia’s current oil reserves are also a concern. It is imperative that the country invest in finding new oil and gas wells and investigate exploiting nontraditional production wells.

Given its geographical position, diversity of agricultural products, and reasonable labor costs, Colombia can be competitive in developing its food, beverage, and consumer products industries, as long as it is committed to the necessary investment and research. The agricultural sector, which provides raw materials for the country’s consumer products industry, also requires ongoing investment. The required economic investments, which offer a path to prosperity for Colombia, are of a manageable size and do not require taking on excessive debt. It may also be possible to find national and international investors willing to assume the moderate risk of these sectors.

Literature Cited

- Agencia Nacional de Hidrocarburos, “Producción Fiscalizada de Crudo 2015,” www.anh.gov.co/Operaciones-Regalias-y-Participaciones/Sistema-Integrado-de-Operaciones/Paginas/Estadisticas-de-Produccion.aspx (2015).

- Gutiérrez, R. A., “Origins and Development of the Chemical Industry in Colombia,” Editora Guadalupe Ltda., Bogotá, Colombia (2006).

- Documento Petróleo Energético, “60 Years of Ecopetrol, a New Axis of Power and Wealth in Colombia,” www.documentopetroleoenergetico.com.co/___pdf/sep_ecopetrol2.pdf (2011).

- Institutional Colanta, “Historia,” www.colanta.com.co/institucional/historia (2016).

- National Administrative Department of Statistics, “National Manufacturing Survey,” www.dane.gov.co/index.php/construccion-en-industria/industria/encuesta-anual-manufacturera-eam (2014).

- Ministry of Foreign Trade, DANE – DIAN Cálculos OEE MINCIT, “Colombian Exports January to December 2014,” www.sice.oas.org/ctyindex/col/Exports_2014_s.pdf (2014).

- Vademécum de Mercados, “La Nota Económica,” www.lanotaeconomica.co (Aug. 2015).

1

Copyright Permissions

Would you like to reuse content from CEP Magazine? It’s easy to request permission to reuse content. Simply click here to connect instantly to licensing services, where you can choose from a list of options regarding how you would like to reuse the desired content and complete the transaction.